TAIPEI, Taiwan, March 22, 2021 /PRNewswire/ —Appeal of in-person branch banking fading fast post pandemic

Highlights:

- 71 percent of Taiwanese consumers prefer to use digital channels to engage with their bank during financial hardship.

- 31 percent of Taiwanese prefer to communicate using their mobile banking app; 22 percent preferred to use internet banking.

- 24 percent of Taiwanese prefer to deal with just one primary bank with a further 40 percent saying that they ‘somewhat agreed’ this was their preference.

A recent survey by global analytics software firm FICO has revealed that 71 percent of Taiwanese consumers prefer to use digital channels to engage with their bank during financial hardship. The poll conducted in December 2020, during the height of the global COVID-19 pandemic, demonstrates the willingness of consumers to embrace digital banking and the opportunities that exist for banks to further develop their offering.

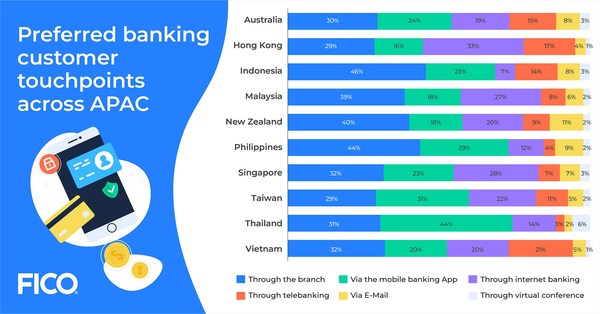

The high level of smartphone penetration in Taiwan meant that 31 percent of Taiwanese preferred to communicate about hardship using their mobile banking app; 22 percent wanted to use internet banking; 11 percent preferred to use phone banking; 5 percent communicated via email; and 2 percent wanted to use virtual conference technology.

“The risk of infection and social distancing requirements made branch visits less appealing last year, accelerating a shift to digital banking channels globally,” said Aashish Sharma, risk lifecycle and decision management lead for FICO in Asia Pacific. “Being able to deliver and manage numerous channels in line with customer preference and deliver a seamless and engaging experience is a challenge that is here to stay. Investment in customer management and communication tools that span these channels and product silos and can deliver personalization and improved decision making is key to making digital banking a success.”

Customer attitudes to new technology from banks such as debt collection automation can yield some interesting preferences and behaviors.

“It is worth noting that during periods of hardship, some customers prefer to deal with the issue using intelligent, automated online services, such as our FICO® Customer Communication Services (CCS) so as to avoid the embarrassment of talking to an agent about outstanding loans. If customers prefer digital channels during times of hardship, their most difficult time, it seems to me we can expect branch banking to continue its decline.” explained Sharma.

Importance of maintaining banking relationships

Banks still have a data and relationship advantage when compared to fintech challengers. The survey revealed that across Asia Pacific, one in three consumers preferred to have all their banking needs serviced by one bank. In Taiwan this was slightly lower at 24 percent, with a further 40 percent saying that they ‘somewhat agreed’ they would like to deal with just one primary bank.

“Managing multiple bank accounts or finance products with different lenders can often be a complex, time-consuming and costly process for the average banking customer,” said Sharma. “Digital banking users today are looking for greater control and visibility of their financial position.”

When asked about their willingness to try a fintech or challenger bank, 22 percent of Taiwanese said that they were inclined to consider a competitor with a further 47 percent relatively open to the idea.

“To consolidate and strengthen main bank engagement, lenders need to offer digital banking features that compete with the challengers to ensure the stickiness and viability of long-term customer relationships,” added Sharma.

Most appealing reasons to switch banks

When asked about the reasons they would make the switch to a competitor, 42 percent of Taiwanese consumers said their number one reason would be to secure improved personalization and controls in their digital banking service. The poll defined this as the ability to view transaction history, update personal details, reset passwords and other such functions. Interestingly, personalization and control was also the top reason for switching across Asia Pacific (31%).

Other top switching drivers across Asia Pacific were; the ability to control a payment card (set transaction limits, lock/unlock); the ability to set up recurring payments; and improved security features such as biometrics and two-factor authentication.